News

Winter Forecast 2020: Because of a strong rebound in the third quarter, this year’s decline in GDP is similar to the Autumn forecast; the deterioration in epidemiological conditions is shifting the recovery into the second quarter of 2021

In the Winter Forecast IMAD projects a 6.6% decline in GDP for this year. After a deep fall in the second quarter, the economy recovered even more than expected in the third quarter. For the last quarter, we expect a renewed decline, but it will be smaller than in the spring, partly due to the adaptation of businesses and consumers to the new circumstances. We estimate that the economic impact of the second wave of the epidemic will be concentrated mainly on the service sector and less on activities integrated into international trade. Given the strong recovery in the third quarter, the decline in GDP in the year as a whole is set to be similar to that forecast in the autumn, despite the renewed deterioration in epidemiological conditions in the last quarter. Owing to the deteriorated epidemiological conditions, the more pronounced economic recovery is being delayed into the second half of next year. Economic growth in 2021 (at 4.3%) is consequently expected to be lower than predicted in our Autumn Forecast (5.1%). With the retention of some restrictions in Slovenia and its trading partners, the recovery will be gradual and differentiated across sectors. The greatest risk to the realisation of the forecast is still associated with the duration and severity of the epidemic. A longer and stronger second wave of infections with stricter containment measures or possible new waves of infections and thus further major closures of economies will continue to represent the greatest risk to a stable recovery. A gradual and well-planned lifting of measures for mitigating the consequences of the epidemic will also play an important role as epidemiological conditions improve. In the event of a faster permanent improvement in epidemiological conditions or faster-than-expected availability of a vaccine or medicine for widespread use, activity could also recover more rapidly than predicted.

In October the rapid spread of infections led to a reinstatement of stringent containment measures in many euro area countries. The most recent economic indicators suggest that in the last quarter of the year the recovery of activity and sentiment in the euro area has come to a halt in service activities, while activity in manufacturing continues to grow, albeit at a somewhat slower pace. In our forecast we took into account international institutions’ latest forecasts for Slovenia’s trading partners (published by 4 December), which assume that with the gradual easing of containment measures, economic activity could start recovering next year but will remain lower than projected in the autumn forecast. The recovery in the next two years will be limited, given the ongoing fight against the epidemic and high uncertainty. On the other hand, it will be supported by comprehensive financial packages agreed at the EU level, increased public investment and government support for individuals and businesses, and accommodative monetary policies. The depth of this year’s decline and the speed of the recovery in 2021 and 2022 will vary significantly across EU countries, reflecting not only the severity of the epidemic and the strictness of containment measures, but also differences in economic structures and domestic policy responses. A return to pre-pandemic levels on average could be possible only in 2022.

In our Winter Forecast, which was prepared in the first half of December, we project a 6.6% decline in GDP for 2020. After a deep fall in the second quarter, the economy recovered more than expected in the third quarter. Based on the available high-frequency data and confidence indicators for October and November, we estimate that the economic impact of the second wave of the epidemic and of the comprehensive protection and containment measures will be concentrated mainly on the service sector and less on activities integrated into international trade. In most sectors the decline will be smaller than in the spring, partly due to the adaptation of businesses and consumers to the new reality. Due to the closure of activities, an equal or greater decline is expected for catering and accommodation and entertainment, sports, recreational and personal services. “Due to the strong recovery in the third quarter, the decline in GDP in 2020 as a whole is expected to be similar to that forecast in the autumn, despite the renewed deterioration in epidemiological conditions in the last quarter,” explained Maja Bednaš, Director of IMAD, adding: “In the autumn forecast we estimated that the measures adopted until September had mitigated the decline in GDP in 2020 by at least three percentage points. Additional measures, mainly aimed at supporting the labour market, businesses and the health care system, will reinforce this effect somewhat, while also creating the conditions for increased activity next year.”

The contraction of total economic activity will arise from a fall in value added in most activities, which will be most pronounced in catering, recreational, sports, cultural and personal services and hotel accommodation. A somewhat smaller, yet still significant, fall is also expected in transportation, trade and manufacturing activities. Owing to negative external impacts and containment measures both at home and abroad, we expect a significant decline in exports and imports this year. Due to lower demand and the high level of uncertainty that also affects investment decisions, corporate investment will also shrink, both in buildings and machinery and equipment. Public investment is set to strengthen slightly this year. A fall in inventories will also have a significant negative impact on GDP growth. Because of limited movement and supply during the quarantine, when spending was not possible, increased uncertainty and precautionary saving, private consumption will also drop more strongly, although disposable income will remain similar to that last year due to the government’s support measures. On the other hand, government consumption will strengthen in the crisis conditions.

“In the current epidemiological situation we estimate that a faster economic recovery could be possible only from the second quarter of 2021 onwards. Due to a delay in recovery we expect 4.3% economic growth in 2021, which is less than projected in our Autumn Forecast (5.1%),” explained Maja Bednaš. With the retention of some restrictions in Slovenia and its trading partners, the recovery will be gradual and differentiated across sectors. The pace of recovery will continue to depend mainly on the epidemiological situation, the speed at which a vaccine is introduced and the response of policies through measures to mitigate the consequences of the epidemic and restart the economy. We expect that government support will continue to play a key role in creating the conditions for a gradual recovery of the economy by preserving measures to support the labour market and boosting investment, for which EU funds will also be available. “However, it is very important that the lifting of the measures to mitigate the consequences of the epidemic is gradual and well planned and that financial support not only buffers business cycle fluctuations but also to the greatest possible extent addresses future developmental challenges,” Maja Bednaš emphasised. Assuming a gradual stabilisation of economic conditions, we expect 4.4% economic growth in 2022, which is slightly higher than predicted in the Autumn Forecast due to a delayed recovery. In 2022, most activities could reach the levels seen before the epidemic. However, a slower recovery is expected especially for tourism-related activities.

The impact of the epidemic and containment measures on the labour market due to a fall in activity was most pronounced in the second quarter of 2020 (a decline in employment and an increase in unemployment). Over the rest of the year, the negative impacts have been considerably mitigated by the adoption and extension of intervention measures to preserve jobs. Employment is expected to be 1.2% lower this year, while the number of unemployed will be around 15% higher. “Given the deteriorated epidemiological conditions and the current closure of many activities, the recovery of the labour market will be delayed into the second half of next year, assuming a slow improvement in the situation,” Maja Bednaš pointed out, adding: “We expect that government measures will continue to mitigate the negative consequences on the labour market, particularly in the first half of 2021, and that they will be lifted only gradually.”

The downside and upside risks to growth are highly related to epidemiological conditions

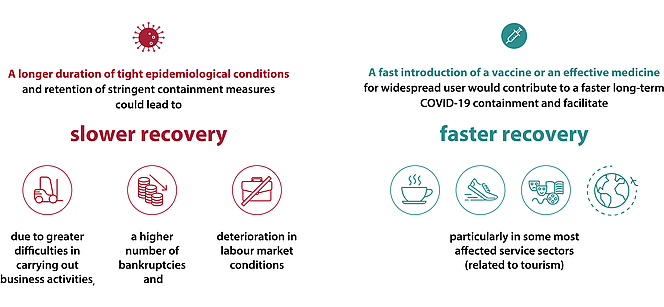

The greatest risk to the realisation of the Winter Forecast remains associated with the epidemiological situation in Slovenia and its most important trading partners. A longer and stronger second wave of infections with stricter containment measures or possible new waves of infections and thus further major closures of economies will continue to pose the greatest risk to a stable recovery. The retention or re-introduction of stringent containment measures would further hamper particularly service activities. In the event of further major business closures, the consequences would also be felt in industry. In deteriorated economic conditions, a premature removal of measures to mitigate the consequences of the epidemic could also lead to higher unemployment and more companies facing difficulties in pursuing their activities. All of this would be reflected in a slower recovery. “However, in the event of a faster permanent improvement in epidemiological conditions or faster-than-expected availability of a vaccine or medicine for widespread use, it is also possible that activity will recover more rapidly, particularly next year”, Maja Bednaš ended on a more positive note.