News

Slovenian economic mirror: A slowdown of economic activity in Slovenia and in the euro area in the first quarter

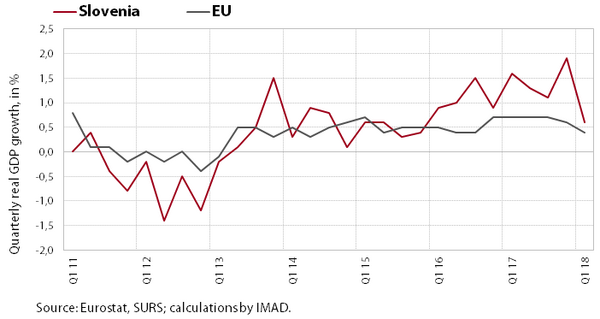

Economic growth in the euro area slowed in the first quarter; owing to uncertainties in the international environment, prospects are less optimistic than in the autumn. Economic growth in Slovenia also eased at the beginning of the year, largely on account of slower growth in foreign demand and unfavourable weather impacts on construction. The labour market situation continues to improve. The number of persons employed is rising and is similar to that in 2008. Year year-on-year wage growth is higher this year than in 2017. Inflation has increased in the last two months. Growth in loans to domestic non-banking sectors remains low.

Economic growth in the euro area slowed in the first quarter; owing to uncertainties in the international environment, prospects are less optimistic than in the autumn. The moderation of quarterly growth (0.4%, seasonally adjusted) was to a great extent attributable to a decline in exports relative to the last quarter of 2017. Year on year, GDP was up 2.5%. Increased uncertainties internationally, particularly due to the announcement (and introduction) of some anti-trade measures by the US and the elevated geopolitical risks in the Middle East, are reflected in a further deterioration of confidence in the euro area economy. Meanwhile, euro prices of oil are rising owing to higher uncertainties on oil markets and the depreciation of the euro against the US dollar.

Economic growth in Slovenia also eased at the beginning of the year, largely on account of slower growth in foreign demand and unfavourable weather impacts on construction. Like in the EU, a significant contribution to year-on-year GDP growth (4.6%) came from domestic consumption, while the contribution of growth in exports of goods and services was smaller than in previous quarters. Growth in private consumption was supported by favourable labour market conditions and high consumer confidence. The relatively strong growth in gross fixed capital formation continued. Government consumption was also slightly higher year on year, largely owing to growth in employment. Exports were up considerably year on year, despite a decline following the strong previous quarter.

Economic growth in Slovenia also eased at the beginning of the year, largely on account of slower growth in foreign demand and unfavourable weather impacts on construction. Like in the EU, a significant contribution to year-on-year GDP growth (4.6%) came from domestic consumption, while the contribution of growth in exports of goods and services was smaller than in previous quarters. Growth in private consumption was supported by favourable labour market conditions and high consumer confidence. The relatively strong growth in gross fixed capital formation continued. Government consumption was also slightly higher year on year, largely owing to growth in employment. Exports were up considerably year on year, despite a decline following the strong previous quarter.

The labour market situation continues to improve. The number of persons employed is rising and is similar to that in 2008. In the first quarter it was up year on year in all private sector activities, in addition to a declining number of unemployed persons, mainly due to the hiring of foreign citizens. Growth in the public sector mainly reflects higher employment in the education and health sectors. The number of registered unemployed persons is declining: at the end of May it was 76,705 persons (12.5%) lower than in May 2017. Year year-on-year wage growth is higher this year than in 2017, in the private sector primarily as a consequence of high economic activity and hence good business results, in the public sector owing to the implementation of agreements with trade unions and regular promotions at the end of last year.

Inflation has increased in the last two months. The stronger year-on-year growth of consumer prices is attributable to both higher energy prices as a consequence of strong oil price growth on world markets and the depreciation of the euro and a significant contribution of certain prices of services. Strong price growth was also recorded for the ‘”recreation and culture" group owing to higher prices of package holidays. The contribution of food prices also remains significant. Prices of semi-durable and durable goods remain down year on year. Core inflation, which otherwise rose slightly in May, continues to hover around 1%.

Growth in loans to domestic non-banking sectors remains low. Corporate deleveraging has risen slightly again. Besides on bank loans, enterprises are also relying on other sources of finance. The relatively strong growth of household loans has eased. Deposits by domestic non-banking sectors continue to expand, but with low deposit interest rates their maturity structure is deteriorating further. Bank deleveraging abroad came to a halt this year. Non-performing loans continue to fall gradually.

The general government balance on a cash basis was positive in the first four months (EUR 100 million). Amid favourable economic developments, general government revenue was significantly higher than in the same period of last year (7.2%). In addition to revenues from taxes (except excise duties) and social contributions, the inflows from the EU budget were also higher year on year, while non-tax revenues were lower. General government expenditure was up 3.8% year on year in the first four months. After stagnation in the first quarter, its year-on-year growth was boosted particularly by higher expenditure on goods and services and stronger growth in expenditure on pensions and the wage bill.