Charts of the Week

Charts of the week from 20 to 24 April 2026: economic sentiment, Slovenian industrial producer prices and average gross wage per employee

The economic sentiment indicator declined in April due to the war in the Middle East and heightened uncertainty in the international economic environment. The most pessimistic responses were recorded among consumers and, within the business sector, in retail trade. In March, Slovenian industrial producer prices increased slightly, while their year-on-year growth slowed, mainly due to a decline in prices on foreign markets. A sharp increase in the minimum wage accelerated year-on-year nominal growth in the average gross wage in January and February, particularly in private-sector activities with a high share of minimum wage earners. In the public sector, growth remained relatively high, mainly due to the implementation of the wage reform.

Economic sentiment, April 2026

The economic sentiment indicator declined in April, reflecting the impact of the war in the Middle East, and fell below its long-term average to its lowest level since the second half of 2023. The deterioration was driven mainly by the consumer confidence indicator, which fell by 10 p.p., marking the largest decline since March 2022. The indicator also decreased in retail trade (by 13 p.p., although it is highly volatile month-to-month) and, to a lesser extent, in manufacturing. By contrast, confidence in service activities increased slightly, while in construction it remained unchanged from the March level. Compared with April last year, all confidence indicators were lower. Relative to the long-term average, the overall indicator and the confidence indicators in retail trade, manufacturing and among consumers remained below their respective averages.

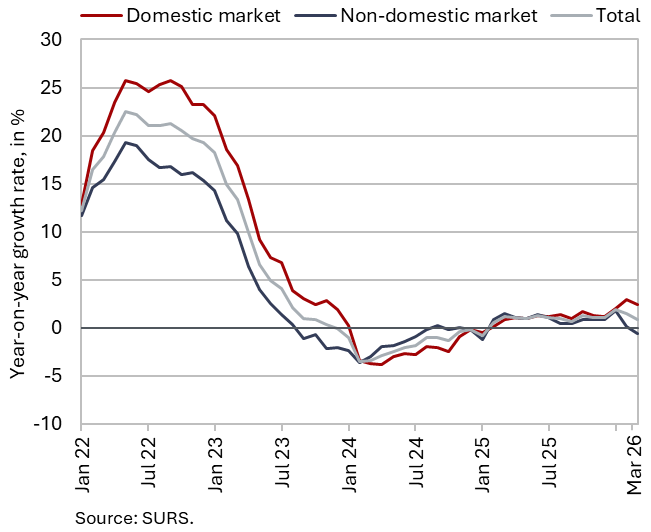

Slovenian industrial producer prices, March 2026

In March, Slovenian industrial producer prices increased slightly on a monthly basis (by 0.2%), while year-on-year growth slowed slightly for the second consecutive month, to 0.9% (from 1.5%). Energy prices were the main factor behind the moderation in year-on-year growth; in March they were lower year-on-year (by 2.8%), reflecting a monthly decline in electricity, gas and steam supply prices (by 5.3%) as well as a higher base effect. Prices of capital goods were also lower year-on-year (albeit marginally, by 0.1%). Year-on-year growth in the prices of intermediate goods slowed by 0.4 percentage points compared with February, to 1.1%. By contrast, price growth in the durable consumer goods group strengthened more markedly (to 5.1%). Price growth in the non-durable consumer goods group continued to gradually slow (to 1.2%). Price growth of industrial products on the domestic market stood at 2.4% in March and, for the second consecutive month, significantly exceeded growth on foreign markets, where prices declined year-on-year (by 0.6%) in March. Price growth on the domestic market exceeded that on foreign markets in all main industrial groups, with the exception of energy.

Average gross wage per employee, February 2026

The year-on-year nominal growth in the average gross wage remained high in February (7.2%): 7.8% in the private sector and 5.9% in the public sector. Growth in the private sector was primarily influenced by a 16% increase in the minimum wage at the beginning of the year. The highest year-on-year wage growth in February was recorded in construction, accommodation and food service activities, and administrative and support service activities (including employment agencies), which are activities with the highest shares of minimum wage recipients. In the public sector, growth remained relatively high, linked to the wage reform involving the agreed increase in base wages at the beginning of last year and to collective bargaining agreements.

In the first two months of 2026, the overall average gross wage increased by 4% in real terms (by 7% in nominal terms) – by 2.8% in the public sector and by 4.6% in the private sector (by 5.7% and 7.5% in nominal terms respectively).