Autumn forecast

Autumn Forecast of Economic Trends 2022

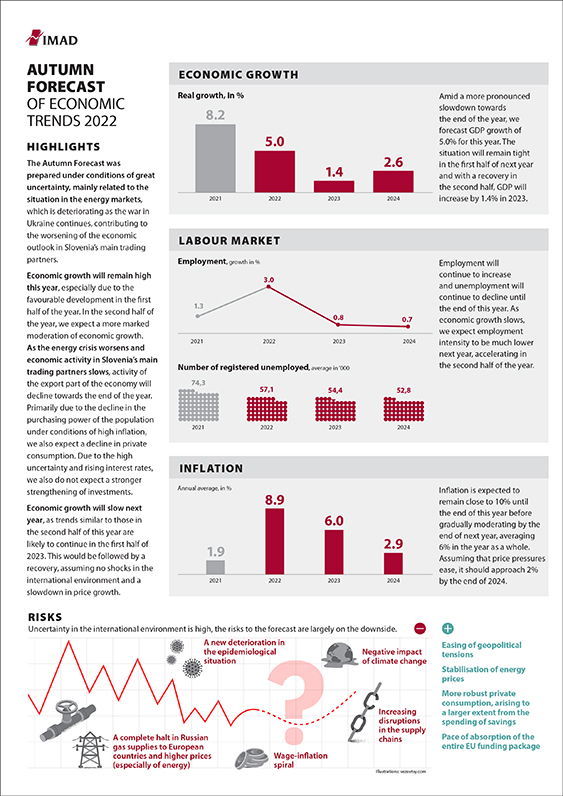

The Forecast was prepared under conditions of great uncertainty, mainly related to the situation on the energy markets, which is deteriorating as the war in Ukraine continues, contributing to the worsening of the economic outlook for Slovenia’s main trading partners. In the Autumn Forecast, IMAD predicts GDP growth of 5% for this year, which is 0.8 p.p. more than was predicted in the spring, mainly due to higher growth in private consumption and the high contribution of inventory changes in the first half of the year. In the second half of the year, we expect a slowdown in the export part of the economy, which is indicated by the deterioration in confidence indicators in the summer months, while forecasts of international institutions have also deteriorated since the spring. We also expect a decline in private consumption, primarily due to the decline in the purchasing power of the population under conditions of high inflation. Amid high uncertainty, high prices and rising interest rates, we do not expect investment to strengthen significantly, despite continued growth in government and housing investment. For 2023, we expect GDP growth of 1.4%, which will largely result from developments in the second half of the year. In the first half of next year, value added in manufacturing and merchandise exports will still be affected by lower growth in foreign demand, lower gas consumption and still high prices. Given the predicted, again somewhat higher growth in Slovenia’s trading partners, as is evident from the currently prevailing forecasts of international institutions, recovery would follow in this part of the economy in the second half of the year. On average, private consumption growth will be significantly lower than this year, due to the impact of inflation on purchasing power and prudent spending on non-essential goods and services. Private sector investment will also remain subdued, with government investment having a positive impact on the level of investment activity. Despite the expected slowdown, inflation is expected to remain high until the end of this year and average around 6% next year, gradually declining towards the end of the year. Employment will continue to increase and unemployment will continue to decline until the end of this year. Next year we expect a significantly lower employment intensity, which is expected to accelerate in the second half of the year. Uncertainty in the international environment is high, the risks to the forecast are largely on the downside and continue to depend heavily on the course of the war in Ukraine and the situation on the energy markets as well as the global epidemic situation. A deterioration of the energy situation and a deeper recession in Germany and Slovenia’s other main trading partners would lead to lower growth in economic activity in Slovenia, which would stagnate or decline slightly if euro area GDP growth is lower than projected (by 2 to 2.5 p.p. compared to the baseline scenario).