Autumn forecast

Autumn Forecast of Economic Trends 2021

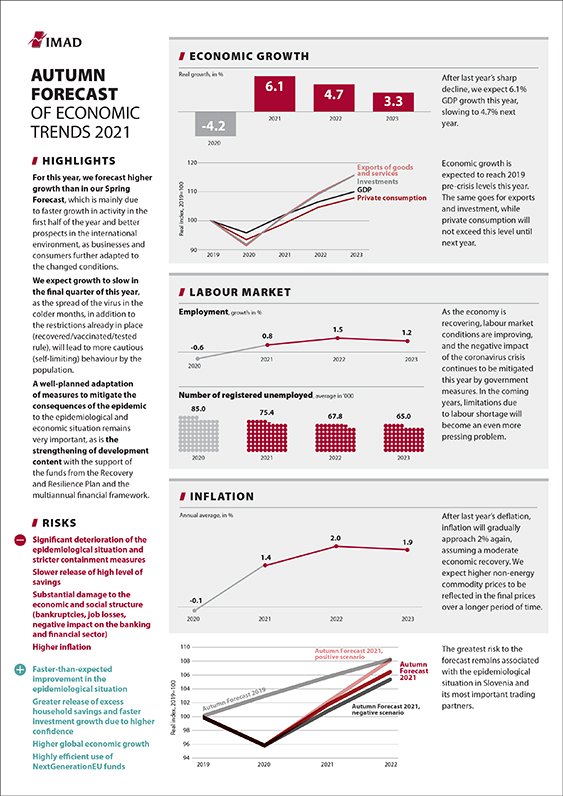

The economic outlook has improved and we expect GDP growth of 6.1% this year. Mainly due to higher forecasts in the international environment, faster-than-expected activity growth, especially in the second quarter and the summer months, and the continued adjustment of businesses and consumers to the changed conditions, our forecast is higher than projected in the Spring Forecast (4.6%). After a sharp decline in economic activity last year (4.2%), the recovery in activities related to external trade (manufacturing and transportation), which began in the second half of last year, continues this year. Export and import trends are favourable and, on the investment side, investment in equipment and machinery in particular is increasing. With the gradual easing of containment measures, turnover in trade increased year-on-year. Accommodation and food service activities, gambling and betting activities and sports, cultural, entertainment and personal care services have also been recovering. Private consumption also increased, mainly due to growth in disposable income, but also to the gradual use of accumulated savings, which rose sharply over the past year. At the same time, the household savings rate is expected to exceed the 2019 level in the coming years. Manufacturing and construction, as well services related to these two sectors, will mostly already reach their 2019 levels of activity this year, as will investment and international trade. Other business services and private consumption, which have been hit harder by the epidemic, will mostly reach their pre-crisis levels next year, except tourism-related services that will reach that level later. As the economy is recovering, labour market conditions are improving, and the negative impact of the coronavirus crisis continues to be mitigated this year by government measures. For this year, we expect 0.8% employment growth and a 11% decline in the average number of unemployed, which will be only 2% higher than in 2019. Over the next two years, the economic recovery will continue. In 2022, GDP growth is expected to moderate to 4.7% and to 3.3% in 2023. Labour market conditions will further improve, while limitations due to labour shortage will become an even more pressing problem. Epidemiological situation remains uncertain, which is also the greatest risk to the realization of the forecast. Therefore, it will be very important to adapt the measures to mitigate the consequences of the epidemic to the epidemiological and economic situation, as well as to strengthen development content with the support of the funds from the Recovery and Resilience Plan and the multiannual financial framework. These are the key findings of the Autumn Forecast of Economic Trends presented by the Institute of Macroeconomic Analysis and Development (IMAD).