Spring forecast

Spring Forecast of Economic Trends 2021

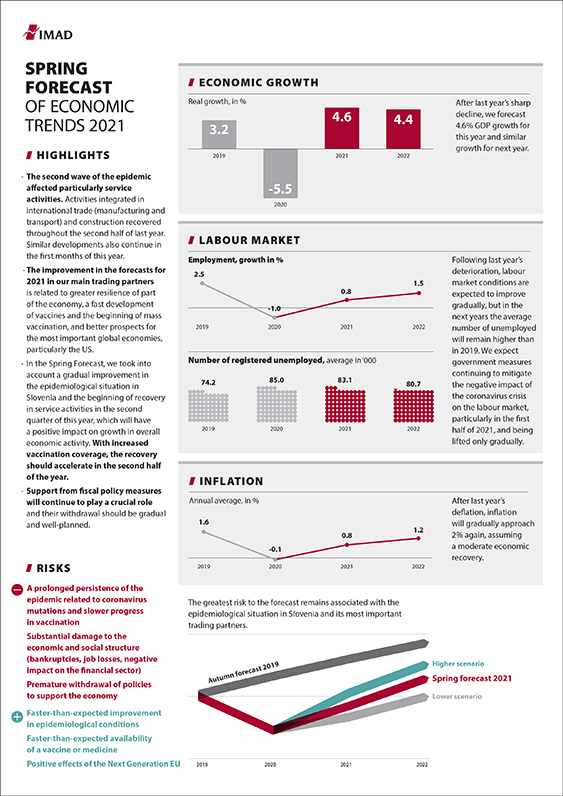

After last year’s sharp contraction of economic activity, we forecast 4.6% GDP growth for this year. Assuming an improvement in the epidemiological situation and a gradual increase in vaccination coverage, the recovery should start in the second quarter and accelerate in the second half of the year – these are also the assumptions of the central forecasts for main trading partners. Particularly because of better prospects in the international environment and a smaller negative impact of the epidemic on the export-oriented part of the economy and construction during the second wave, the forecast is somewhat higher than projected in the Winter Forecast (4.3%). Economic recovery will remain differentiated across sectors. We expect further growth in manufacturing and construction, as well as in related service activities. Similarly, we also expect relatively strong growth in investment, especially in infrastructure and housing. With a gradual opening of service activities, private consumption will also start picking up in the spring, reflecting growth in disposable income, but also a release of accumulated savings and hence a gradual decline in the household saving rate. Growth in external trade will continue as well, particularly for goods and gradually also for most segments of services. The slowest and longest recovery is expected in tourism-related services. With the easing of epidemiological conditions, employment will continue to recover gradually this year, while unemployment will remain similar to that last year in the year as a whole. We expect government measures continuing to mitigate the negative impact of the coronavirus crisis on the labour market, particularly in the first half of 2021, and being lifted only gradually. In the next two years, economic recovery is expected to continue: in 2022, GDP growth will be similar to this year (4.4%), while in 2023, it will be 3.3%. Employment growth will continue to strengthen amid the expected further economic recovery, but the annual average number of unemployed in 2023 will remain higher than in 2019. Epidemiological conditions remain uncertain. This is the greatest risk to the forecast, which will be highly dependent on the progress of the epidemic and the implementation of the vaccination strategies in Slovenia and other countries. Among the risks to the forecast, which are somewhat more balanced than last year, negative risks still predominate. A gradual and well-planned lifting of measures to mitigate the consequences of the epidemic and a transition to their development component within the National Recovery and Resilience Plan and the Multi-annual Financial Framework 2021–2027 will also play an important role.