Charts of the Week

Charts of the week from 19 to 23 February 2023: economic sentiment, average gross wage per employee, Slovenian industrial producer prices and other charts

Economic sentiment remained unchanged in February and deteriorated compared to a year ago. In January, Slovenian industrial producer prices rose for the first time since April last year but were lower year-on-year due to the base effect. The average gross wage per employee rose more strongly in real terms in December (by 4.4%) than in the previous months, also under the influence of weakening inflation, and by an average of 2.2% in 2023. The nominal value of fiscally verified invoices rose by 5% year-on-year between 4 and 17 February 2024, similar to the average for the last quarter of last year and for January.

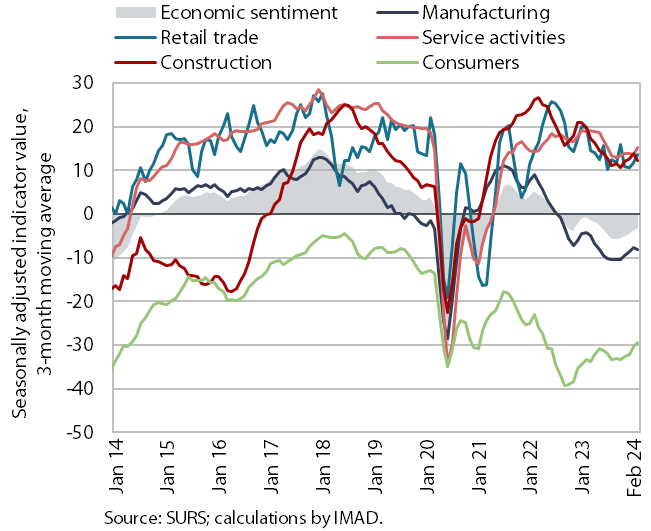

Economic sentiment, February 2024

The economic sentiment indicator, which started to improve in November 2023, remained almost unchanged in February, while it was lower year-on-year. Only in services did the confidence indicator improve compared to January. Compared to February 2023, confidence was down in all segments except among consumers, although here it is still significantly more below the long-term average than in the years before the epidemic. The year-on-year lower values of most confidence indicators point to a continuation of weak activity dynamics.

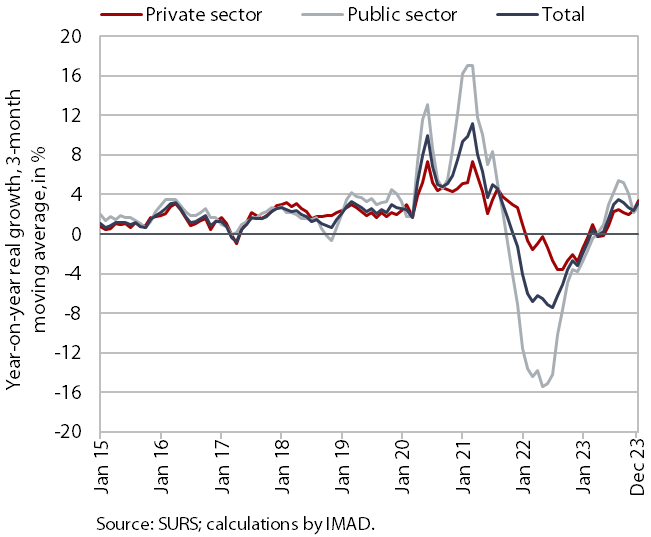

Average gross wage per employee, December 2023

Amid lower inflation, the year-on-year growth in the average gross wage in December 2023 (4.4%) was higher in real terms than in the previous months. In the private sector, growth in December (3.7%) was higher than on average in 2023. It was highest in administrative and support service activities, accommodation and food service activities and construction, which are facing the greatest labour shortage. Growth in the public sector (5.6%) was also higher than in previous months, partly due to public servants' promotion raises at the end of the year and to the performance-related bonus payments for regular work. In 2023, the average year-on-year gross wage growth was 2.2% in real terms (1.9% in the private sector and 2.7% in the public sector).

Nominal year-on-year growth in the average gross wage was slightly higher in December (8.7%) than in November but lower than in previous months. Growth was 8% in the private sector and 10% in the public sector. In 2023, the average year-on-year growth was 9.7% (9.4% in the private sector and 10.3% in the public sector).

Slovenian industrial producer prices, January 2024

Slovenian industrial producer prices, which had been falling month-on-month since April last year, rose by 0.2% in January, while they were 1% lower year-on-year. Prices rose month-on-month in most product groups (most significantly in energy products by 0.9%), while prices of capital goods fell slightly (by 0.1%). Despite the monthly increase, producer prices were lower year-on-year (for the first time since December 2020) due to the base effect, falling by 1%. Prices of intermediate goods were lower (by 4.7%) and price growth in other groups slowed further, to about 2.5%. Slovenian producer prices on foreign markets were 2.3% lower year-on-year and growth in the domestic market slowed to 0.3%.

Value of fiscally verified invoices, in nominal terms, 4–17 February 2024

The nominal value of fiscally verified invoices between 4 and 17 February 2024 was 5% higher year-on-year. After growth halved in the previous 14-day period, the year-on-year growth in total turnover and turnover in trade, which accounted for almost 80% of the total value of fiscally verified invoices, strengthened year-on-year to 5%, which is in line with the average for the last quarter of last year and the average for January. There was a strong increase in growth in the sale of motor vehicles (from 3% to 10%) and a slight increase in retail trade (to 6%), while the year-on-year decline in wholesale trade slowed slightly (to 5%). Year-on-year turnover growth in accommodation and food service activities, certain creative, arts, entertainment, and sports services, and betting and gambling was similar as in previous 14-day periods (overall growth in accommodation and food service activities and in other service activities was 8%).