Charts of the Week

Charts of the week from 22 to 26 January 2024: economic sentiment, value of fiscally verified invoices and average gross wage per employee

Economic sentiment continued to improve slightly month-on-month in January, but remained lower than a year ago and below the long-term average. In mid-January, the value of fiscally verified invoices was up 6% year-on-year in nominal terms. The largest contributions to growth came from the retail trade and the sales of motor vehicles. Year-on-year real growth in the average gross wage was slightly higher in November (3.1%) than in the previous months, which is attributable to higher growth in the private sector (4.2%). In the first eleven months, the average gross wage was 1.9% higher year-on-year in real terms (9.8% in nominal terms). The increase in the public sector was more pronounced than in the private sector.

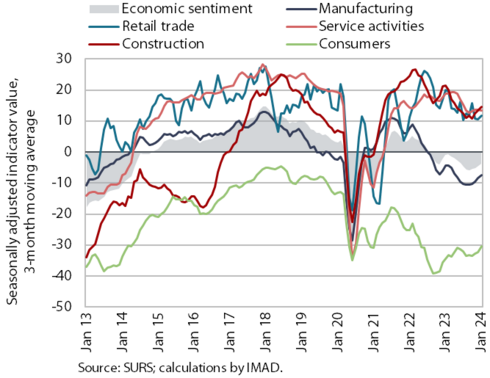

Economic sentiment, January 2024

The economic sentiment indicator increased slightly month-on-month in January for the third month in a row, while it was still down year-on-year. Compared to the previous month, confidence rose in retail trade and among consumers, but fell in manufacturing, services and construction. This reflects a continued uncertain economic situation at the beginning of this year related to weak domestic and foreign demand and labour market slack. Compared to January 2023, confidence was down in all segments except among consumers, although here it is still significantly more below the long-term average than in the years before the epidemic.

Value of fiscally verified invoices, in nominal terms, 7–20 January 2024

The nominal value of fiscally verified invoices between 7 and 20 January 2024 was 6% higher year-on-year. Growth was similar to the average for the fourth quarter of last year, when it had increased compared to the second and third quarters. Similar turnover growth was recorded in trade (5%); in retail trade it doubled to 8%, in the sales of motor vehicles it declined, although it remained strong (9%) and in wholesale trade it declined by 7% year-on-year (it was 1% higher year-on-year in the fourth quarter of last year on average). Year-on-year turnover growth in accommodation and food service activities, certain creative, arts, entertainment, and sports services, and betting and gambling was slightly lower than in the last quarter of 2023 (overall growth in accommodation and food service activities and in other service activities was 8%).

Average gross wage per employee, November 2023

Year-on-year growth in the average gross wage was slightly higher in real terms in November (3.1%) than in the previous months, which is attributable to higher growth in the private sector (4.2%). In addition to lower inflation, the year-on-year increase in real wage growth was also influenced by payments in the private sector (13th month payments and Christmas bonuses), which were higher than in November 2022. Growth was highest in accommodation and food service activities, which (along with construction and administrative and support service activities) is one of the sectors with the greatest labour shortages. In the public sector, it was 1% and therefore lower than in previous months. The lower growth is linked to a higher base last year due to a wage increase in October 2022. At 8.1%, nominal year-on-year growth in the average gross wage in November was slightly lower than in previous months. Growth was 9.3% in the private sector and 5.9% in the public sector. In the first eleven months, year-on-year gross wage growth was 1.9% in real terms (1.7% in the private sector and 2.3% in the public sector). Year-on-year nominal growth in the same period was 9.8% (9.6% in the private sector and 10.3% in the public sector).