Charts of the Week

Charts of the week from 8 to 12 April 2024: electricity consumption by consumption group, production volume in manufacturing and current account of the balance of payments

Electricity consumption in the distribution network was lower year-on-year in March in all consumption groups. Manufacturing output continued to increase in February. Since the beginning of the year, it has risen in all industry groups according to technology intensity. In the first two months, it was on average also slightly higher year-on-year. The current account surplus remained high in the last 12 months (up to February).

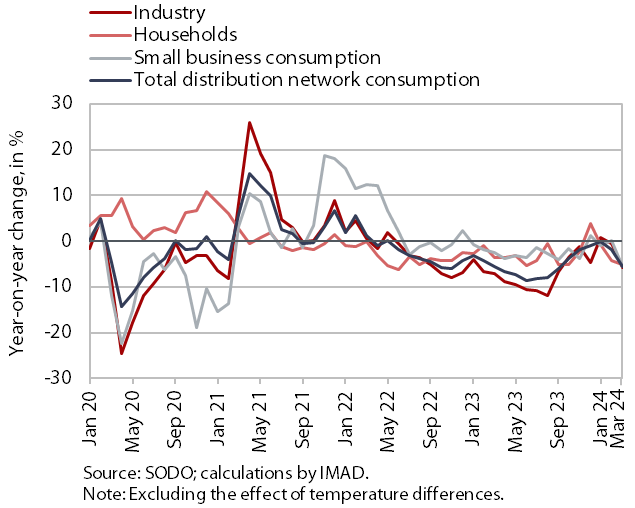

Electricity consumption by consumption group, March 2024

In March, electricity consumption in the distribution network was lower year-on-year in all consumption groups. Household consumption was 5.1% lower year-on-year, which could also be due to the lower occupancy of tourist accommodation facilities at the ski resorts, which operated only to a limited extent due to the high temperatures. Industrial consumption and small business consumption were also lower year-on-year in March (by 5.7% and 5.6% respectively), partly due to two fewer working days.

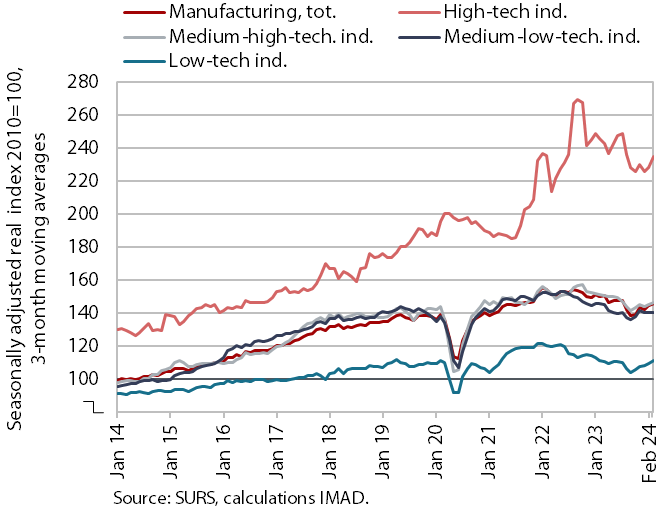

Production volume in manufacturing, February 2024

Manufacturing output continued to rise in February and was higher year-on-year. Since the beginning of the year, manufacturing output has risen in all industry groups by technology intensity. In the first two months, it was also higher year-on-year (by 0.7%). Activity in the energy-intensive chemical industry and the manufacture of other non-metallic mineral products and in some less technologically demanding industries (repair and installation of machinery and equipment, manufacture of rubber products, wood-processing and furniture industries, manufacture of leather and textiles) remained lower than a year ago. However, activity in the energy-intensive manufacture of paper and basic metals was higher year-on-year in the first two months.

According to data on business trends, manufacturing companies’ expectations regarding future production have improved since the beginning of the year. However, inventory indicators remain lower than a year ago. In particular, the level of (total and export) orders was low at the end of the first quarter. Companies continue to cite insufficient foreign and domestic demand as the main limiting factor (one third of respondents).

Current account of the balance of payments, February 2024

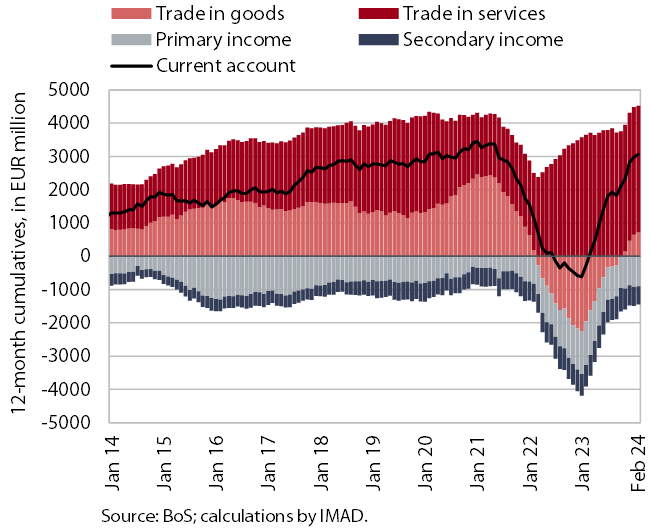

The current account of the balance of payments recorded a large surplus of EUR 3.1 billion in the last 12 months (up to February), compared to a deficit of EUR 269.3 million in the same period a year earlier. The main reason for the shift to a surplus was the goods trade balance, as imports of goods have fallen more sharply than exports. The surplus in trade in services widened further, particularly in trade in processing, construction and transport services. The deficits in the primary and secondary income balance have narrowed. The former decreased due to lower net outflows of income from equity capital (dividends and profits) and higher net interest receipts by the Bank of Slovenia from deposits in foreign accounts. The lower secondary income deficit resulted from lower net outflows of private sector transfers.